Questions About Tariffs

March 21, 2025

To Inform:

The Joseph Group had the great privilege (and a lot of fun!) hosting a crowd of clients and friend at our March Portfolios and Pints this past Tuesday in Hilliard. Joseph Group Partner and CEO Travis Upton and I fielded “questions from a hat” that had been submitted by clients and advisors. One question that we’ve gotten quite a bit over the last couple of months is the issue of trade tariffs and the implications they may have for markets.

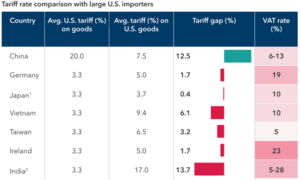

To address the question of tariffs, let’s first try to understand the why behind them. President Trump has gone on the record many times over the last several decades expressing a view that free trade has been a boon for America’s trading partners and a raw deal for the United States. Whether you agree with the president or not, I think we can all agree that free trade involves tradeoffs. US consumers had access to cheap goods by importing them from countries around the world with low labor costs. The tradeoff was that US manufacturing jobs shrank or as was the case in some industries, disappeared altogether. The chart below from Capital Group shows the average tariff rate on imports of US goods for several key trading partners across the world. Many of them levy significantly higher tariffs on imports than does the United States and, when combined with value-added taxes, are a major disadvantage for US companies.

Source: Capital Group

The next chart from Capital Group suggests there are four different scenarios or motivations that could be informing the Trump Administration’s views on trade. It seems that the administration is seeking a variety of outcomes with trade policy. There is indeed a “funding” element to all of this – the president has spoken of a desire to attempt to balance the budget but also wants to extend 2017’s Tax Cut and Jobs Act. The idea of “rebalancing” also seems to track with what we’ve seen so far. The administration has focused specifically on some of the industries impacted under this scenario including steel, aluminum, and pharmaceuticals. We think permanent decoupling and negotiating are considerations but are being used as means to an end, not the primary goal given statements made by members of the administration. Interestingly, negotiations are already happening on the margins. Vietnam, who the US has a large trade deficit with, is preemptively reviewing some of their trade policies in what many view as an attempt to avoid future tariffs.

Source: Capital Group

Ultimately, we think businesses adjust and outcomes may vary. Companies and industries that rely heavily on imports of raw goods may need to shift supply chains or reshore production. We’re already seeing evidence of adjustment and impacts as a large pharmaceutical company announced this morning plans to spend more than $55 billion in the US over the next four years to avoid the risk of tariffs on imported drugs. Companies and industries with large exports to foreign countries may face retaliation effects as we’ve already seen with US distilling companies seeing their liquors destocked from the shelves of stores in Canada.

We believe that the balanced approach we take to getting stock exposure in client accounts is the best way to navigate this environment. One example of this is what we’ve seen this year in our Home Grown portfolio. This portfolio invests in many Ohio companies as well as a number of large US blue chip stocks. The best performers year-to-date are ones we feel are relatively insulated from the effects of a trade war. A couple of top performers are pharmaceutical which have posted returns greater than 20% so far this year. Eventually this near-term uncertainty will pass, and investors and companies will understand the hand of cards they’ve been dealt. We have little influence over the hand we’re being dealt, but that doesn’t matter. What matters is how we play that hand.

Written by Alex Durbin, CFA, Chief Investment Officer