Three Things We Are NOT Seeing in the Markets

March 28, 2025

To Inform:

Federal Reserve Chair Jerome Powell summed up the current environment well in a recent press conference:

“The new Administration is in the process of implementing significant policy changes in four distinct areas: trade, immigration, fiscal policy, and regulation. It is the net effect of these policy changes that will matter for the economy and for the path of monetary policy. While there have been recent developments in some of these areas, especially trade policy, uncertainty around the changes and their effects on the economic outlook is high.”

We’ll emphasize the word uncertainty. John Authers, who writes a daily piece for Bloomberg included the charts below in his piece on March 28. An index of “Global Uncertainty has increased dramatically in recent weeks with news on tariffs and trade, but the chart below shows the “VIX,” an index of stock market volatility derived from options trading, is below 20, indicating little stress in the stock market. If stock markets were sniffing out something more sinister, the VIX would likely be elevated…but that’s not happening.

Source: Bloomberg, March 28, 2025

As we seek to get our arms around the current uncertain environment, we believe it is instructive to look at what we are NOT seeing in the markets. Here are three observations we think are important:

We are NOT seeing signs of stress in credit markets.

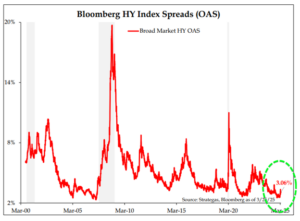

Credit spreads, or the amount of interest over and above government bond rates which reflects the risk of corporate bonds defaulting or going bankrupt, remain close to historic lows. Strategas Research Partners bond guru Tom Tzitzouris says, “high yield spreads show no indication of stress to come – they are like the honey badger, they just don’t care.”

Source: Strategas Research Partners

The chart above shows high yield bond spreads over the last 25 years. Spikes such as the Global Financial Crisis in 2008 and COVID in 2020 are notable, while today’s level remains close to historic lows. Tzitzouris says, “for reference, historically, the shallowest of recessions typically translates to spreads of about 7%.” The current level of 3% isn’t even close – we’d have to see this move a lot more to reflect broader economic concerns.

We are NOT seeing dramatic moves in interest rates.

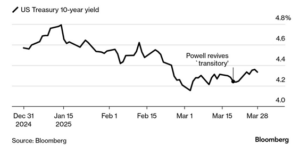

In general, if the market thought tariffs were going to cause a spike in inflation, longer term interest rates would likely rise significantly. On the other hand, if the market thought shifts in trade policy were going to drive the economy into recession, interest rates would likely fall significantly. We’re not seeing either.

The chart below shows the rate on the 10-year Treasury since the beginning of the year and shows the 10-year rate has generally traded in a range of 4.2% to 4.8%. While that range is not insignificant, it’s not giving a dramatic signal either.

Source: Bloomberg

It’s also worth noting expectations for the Federal Reserve, which controls short-term interest rates, has also remained stable. The market is currently pricing in two 0.25% rate cuts to short-term interest rates for the remainder of 2025, with the first most likely to come in June.

Relatively stable interest rates have meant bonds have acted as a ballast for portfolios with the Bloomberg Aggregate Bond Index up about +2% year-to-date through March 27.

We are NOT seeing wholesale liquidation of stocks.

We believe recent volatility in the major stock indexes has reflected more of a leadership rotation than a mass liquidation. As you can see in the chart below, “Growth” stocks (think big technology and computer chips) have been the biggest decliners amidst the recent volatility while “Value” stocks (think dividends, sectors such as health care, financials) have held up relatively well.

Source: Bloomberg

In recent meetings, Joseph Group Chief Investment Officer Alex Durbin, has shared what this “leadership rotation” has meant inside of the “Home Grown” individual stock portfolio strategy we have the privilege of managing for clients. While we are seeing some big technology stocks struggle, we also have stocks in the portfolio which are up double digits on a year-to date basis. These stocks are generally coming from more “value” oriented sectors including health care, telecommunications, insurance, and energy.

The current environment is definitely uncertain and with looming tariff deadlines still ahead of us, we would expect more day-to-day volatility. However, if we step back and look at some of the big “potential red flags” which would point to the market heading toward something more sinister, we simply are not seeing it.

Written by Travis Upton, Partner and CEO