Inflation – Looking Past Today’s Impacts

October 22, 2021

To Inform:

If you pick up any newspaper or turn on a financial news channel you won’t have to wait very long to see something about inflation, supply chains, and shortages. We’ve all heard about the spectacular increases in used car prices, shortages in super markets, and a housing market that has defied expectations over the last 18 months. In today’s WealthNotes we’re going to try to get past the immediate headlines and consider an important but perhaps less obvious impact of a rise in inflation.

Common industry parlance includes mention of the “60/40” portfolio. The 60/40 portfolio is shorthand for a portfolio allocated 60% to stocks and 40% to bonds. A portfolio following this strategy has worked quite well for the last 40 years. As the chart below illustrates, stocks have enjoyed a wonderful environment beginning in 1980 in which the earnings yield on S&P 500 stocks has fallen from 15% to just under 5% today. Earnings yield is simply the ratio of earnings to stock prices. As a general rule, owning higher yielding assets leads to higher expected returns over the long run. Put another way, investors in 1980 were paying 6-7 times earnings for stocks, versus something like 21-22 times earnings today.

Source: Yardeni Associates

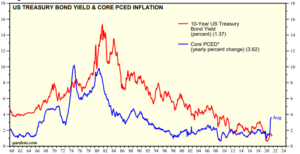

While stocks turned in impressive performances over this time period, bonds were nearly equally as attractive. As a reminder, when yields on bonds fall their prices go up. The chart below shows the decline in the US 10-Year Treasury Bond Yield from north of 15% to today’s level of around 1.5%.

Source: Yardeni Associates

The impact of this twice-blessed environment is best expressed this way: beginning in 1980 a $10,000 investment in a 60/40 portfolio of US Stocks and US 10-Year Treasury Bonds, rebalanced annually, would be worth over $600,000 today (ignoring the impact of taxes and fees).

If you’ve come along with me this far you may be wondering, “That’s great, Alex, but what does it have to do with inflation?” The answer is quite a lot. Rising inflation often sparks an increase in interest rates and an increase in earnings yield. While we can only make forecasts, it isn’t unreasonable to posit that inflation runs hotter in the 2020s than it did in the 2010s. We don’t need a return to 1970s level inflation to see the kinds of negative real returns investors experienced that decade in stocks (-1.5%) and 10-Year Treasury Bonds (-1.21%).

An old adage that’s often used around here is “history doesn’t repeat itself, but it often rhymes.” We don’t think we’re necessarily in for a period of double-digit inflation rates, but we do agree with those who think inflation can run a little hotter than we’ve all been accustomed to (something the Federal Reserve has told us they’d be willing to tolerate!). Our task, as always, isn’t to ask “what’s been working lately?” but to ask, what might do well if the world looks different? Asset classes that historically have done well in inflationary environments include commodities, real estate, and select areas of the stock market (companies with pricing power, financials, energy, small caps).

While the potential end of this Goldilocks era of falling bond yields and rising stock prices poses challenges to investors, in need not spark fear. I’ve always thought it wise to “play the market you’re given, not the one you want.” Inflation makes it likely the future may not look like the past. This means we may need to do things differently, and the objective-based portfolios we have the privilege of managing for clients incorporate these thoughts, seeking to meet objectives regardless of a changing economic environment.

Written by Alex Durbin, Portfolio Manager

Written by Alex Durbin, Portfolio Manager