Markets Climbing a “Wall of Worry”

April 10, 2026

To Inform:

I had the chance this week to sit with some astute investors and clients of The Joseph Group, as well as a portfolio manager of a high yield fund held in many client accounts. We got to talking about some of the big issues being debated in markets today and touched on inflation and recession odds, particularly in light of some of the recent headlines around war with Iran.

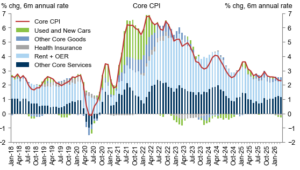

Let’s start with the question of inflation. Today, the Bureau of Labor Statistics released its monthly inflation report. The “headline” inflation number showed an increase of 0.9% month over month, which is an eye-popping number. This was driven almost entirely by energy price inflation, as those rose 21% month over month. What’s interesting to us, though, is that core inflation (inflation stripping out food and energy) was up just 0.2% month over month, below forecasts of 0.3%.

Source: Goldman Sachs

Why is this important? If core inflation (automobiles, insurance, rent, other services) was marching steadily higher as it did in 2021 and 2022 then the economy might be in for some trouble. Core inflation moving beyond the Federal Reserve’s 2% target would argue for further interest rate increases, which tend to be difficult for the market to digest. Looking at today’s data – despite the rise in energy prices – we’re not there.

On the question of recession odds, it is very easy to look at the headlines and think “this is it!” War and energy price inflation can’t be good for the economy, can they? I would say no, but the question isn’t “what is good for the economy?”, the question is “are we headed into recession?” In 2022 we saw a lot of things that weren’t good for the economy. A stock market selloff, war in Ukraine, rising interest rates, rising energy costs, and inflation approaching 10% were a series of factors that had many in the financial press calling for a recession that never came.

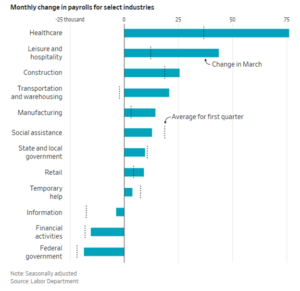

We continue to look at the labor market as a signal for the health of the economy, and despite more muted hiring in recent months, we aren’t seeing the kind of deterioration that presages a recession. Last week’s March jobs report showed 178,000 jobs added to the U.S. economy. Where those jobs were added matters. We saw gains in sectors like construction, transportation, and manufacturing. These are sectors that are typically cutting jobs in a recessionary environment.

Source: The Wall Street Journal

We think that the U.S. can weather the storms of higher inflation and conflict with Iran because the economy has seen these sorts of challenges before and has navigated them with resilience. Despite a barrage of negative headlines, the data simply isn’t showing us that inflation or the jobs market have gotten to the point where the economic expansion we’ve been in since 2020 shows any signs of ending. It’s often said that markets “climb a wall of worry.” That wall might look steeper right now, but we think ultimately the climber can make it over this set of challenges.

Written by Alex Durbin, CFA, Partner and Chief Investment Officer