Weaker Dollar, Stronger Foreign Stock Performance

August 7, 2020

To Inform:

One of the hot topics we discussed at last week’s Portfolios at Your Place was the weaker U.S. dollar and how it was impacting changes in leadership across asset classes. Chris Verrone, Head of Technical Analysis at Strategas Research Partners recently said “there’s no shortage of moving parts in this environment and at the top of that list is the continued weakness from the U.S. dollar.”

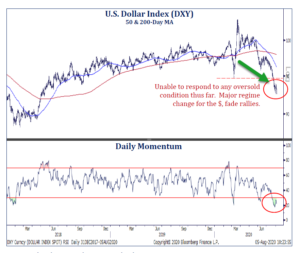

The chart below shows the U.S. dollar index for the past three years. After getting stronger in the spring of 2018, the value of the dollar relative to other currencies was somewhat range bound throughout 2019, had wild swings (like everything else) when COVID-19 hit in March, but has had a clear downward trend since June.

Source: Strategas Research Partners

We believe the weaker dollar has important implications for asset class leadership. First, commodities (i.e., oil, copper, gold) all over the world are priced in U.S. dollars. When the dollar is weaker, it takes more dollars to buy those commodities, so the dollar price of the commodities goes up, resulting in higher returns for commodity investors. Second, a weaker dollar is a tailwind for foreign stock performance. Historically, not only do foreign stocks themselves tend to perform well in a weaker dollar environment, but the currency impact gives an additional lift. When a U.S. investor earns returns in a foreign currency (i.e. Euros, Yen) and the value is converted back into weaker U.S. dollars, the investor ends up with more dollars and therefore a higher return.

We took the chart below from Yahoo Finance looking at the returns for the S&P 500, commodities, and emerging market stocks from June 1 through August 6, corresponding with the period the dollar has been weakening. As you can see from the chart, commodities (green) and emerging market stocks (purple) have outperformed the S&P 500 (blue) during the period of dollar weakness.

Source: Yahoo Finance

One final point. I had a discussion yesterday with a client and she asked, “I heard on the news the dollar is collapsing and some terrible financial calamity is going to happen, is that true?” Just like other asset classes, the U.S. dollar goes through trends and cycles, many of which we have seen before. Look again at the first chart – the current weakness in the dollar is only taking its relative value back to where the dollar was in mid-2018. We could assign multiple fundamental reasons for a weaker U.S. dollar, including lower interest rates and the upcoming U.S. election (politics aside, the dollar has generally been strong under Trump). The U.S. dollar is, and is poised to remain for the foreseeable future, the standard for international reserves. The important thing for investors is how the current macro shifts are impacting asset class leadership.